Different Types of Real Estate Loans and How They Work

Introduction:

In today’s African property investment loans market - where opportunities are rising from Douala to Nairobi - understanding Real Estate Loans isn’t just helpful; it’s the most important financial skill you can develop. It’s the step that separates guesswork from smart investing, fear from confidence, and missed chances from generational wealth.

Think of this property financing guide as a personal workshop - your seat across the table from a seasoned mentor who has walked many African buyers and investors from “I’m not sure how loans work” to “I made the best financial decision for my future.”

When you understand Cameroon mortgage options for loans, you avoid costly mistakes, negotiate better terms, and choose the path that protects your income, property, and peace of mind. And in a market like Housing Finance Cameroon, where it is still evolving, this clarity matters more than ever.

Let’s unpack these concepts together, simply, patiently, and practically.

Residential vs. Commercial Real Estate Loans

Fixed-Rate Loans

A fixed-rate loan works exactly like buying a full sack of garri at a price the seller promises will never change, even if the market price jumps the next day.

With these Real Estate Loan types, your interest rate stays constant from day one until the loan is fully repaid.

Why African Buyers Like It:

-

Predictable monthly payments

-

Protection from inflation

-

Ideal for salaried earners or long-term homeowners

Adjustable-Rate Loans

An adjustable-rate loan is similar to buying fuel, where prices fluctuate weekly. The interest rate moves based on the economy and lender policies.

Why It Can Still Work in Africa:

-

Lower initial rates (good for short-term plans)

-

Investors who plan to sell or refinance quickly can benefit.

A Word of Caution:

In markets with fluctuating currency values or inflation - common in many African countries - adjustable loans require careful planning.

Conventional Mortgage Loans Options Explained

These are traditional Real Estate investment Loans offered by banks and recognized lenders. They follow clear rules and are best suited for buyers with stable income, verifiable documents, and good credit history.

In the African context:

Due to the difficulties of formal employment and the traditional credit score, cooperative lending, community savings groups (njangi), or partner-based financing are taken by most Cameroonians prior to their qualification for other standard mortgages.

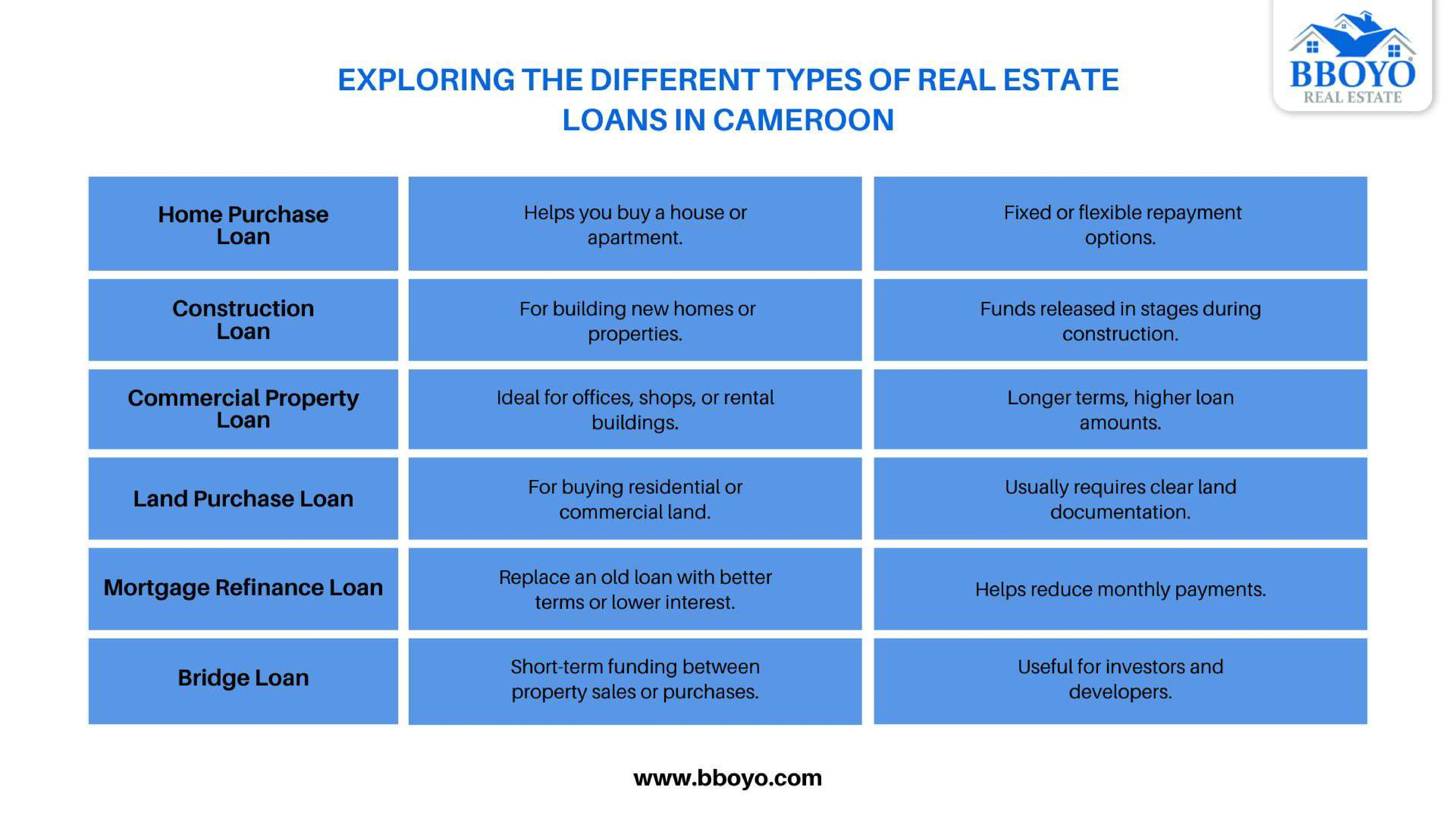

Real Estate Loan Types Every Buyer Should Know in Cameroon

Government-Backed Real Estate Loans (FHA, VA, USDA

While Africa doesn’t have FHA or VA loans exactly like the US, many governments - including Cameroon - have affordable housing initiatives, diaspora mortgage programs, and low-interest loan partnerships with local banks.

These programs:

-

Reduce down payments

-

Lower interest rates

-

Pay attention & motivate young professionals and civil servants to become homeowners.

These loans can be the most affordable in case you are aiming at new housing projects or those estates that have been established by the government.

Bridge Loans and Short-Term Financing Options

Construction financing is are short-term Real Estate loan designed for people building a home from scratch or expanding an existing one.

Picture it like your builder asking for funds in controlled stages - foundation, walls, roofing, finishing - not all at once.

Why They Matter in Africa:

Many Africans prefer building gradually, and these loans support that culture by financing each step as work progresses.

Bridge Loans

A bridge loan is a temporary loan you take while transitioning between properties.

Suppose your current property is yet to sell, and you have discovered a good plot in the growing outskirts of Yaounde. A bridge loan will provide you with rapid capital to avoid the risk.

Perfect for:

-

Emerging cities (Douala, Accra, Kigali)

-

Shareholders with several projects

-

Developers who need short-term liquidity

Residential Real Estate Loans

These are finance homes or rental apartments.

In Cameroon, demand for affordable units, gated communities, and modern apartments continues to rise.

Commercial Real Estate Loans

These finance income-producing properties like:

-

Shops

-

Office buildings

-

Mixed-use structures (common in African cities where people live upstairs and run business downstairs)

Commercial loans often offer larger amounts, but require stronger documentation and a clear revenue plan.

Short-Term vs. Long-Term Loans

Short-Term Loans

Ideal for:

-

Flipping properties

-

Quick renovations

-

Temporary cashflow needs

Long-Term Loans

Best for:

-

Homeownership

-

Large commercial properties

-

Investors seeking stable, predictable payments

Most African banks provide 5–25-year options, depending on income stability and collateral strength.

8. Interest-Only & Balloon Payment Loans

A balloon loan works like paying small amounts on a motorbike for months, then being asked to make one large final payment.

It’s attractive at first because monthly payments are low, but it requires discipline and future planning.

Use with caution:

In emerging markets, unexpected inflation or business slowdown can make the final “balloon” difficult to manage.

9. Owner-Occupier vs. Investment Property Loans

Owner-Occupier Loans

Ideal with new consumers or households. Such loans are usually offered at more friendly rates since they are considered to be low-risk by real estate lenders in Africa.

Investment Property Loans

In case you are targeting rental revenue, Airbnb gains, or the increase in land value, lenders will consider:

-

Cashflow potential

-

Management plan

-

Market location

In cities like Limbe or Buea, where short-stay tourism is growing, these loans are becoming more valuable.

How to Qualify for A Real Estate Loan

Here’s where I speak to you directly as your financial mentor.

In the BBOYO ecosystem, what our lenders really want to see is clarity, stability, and honesty in your financial profile.

Even if your income is non-traditional - like freelancing, agriculture, transportation, or business operations - you can still qualify with the right preparation.

Here’s how to strengthen your loan application:

-

Document all income streams (mobile money statements count!).

-

Show consistency over 6–12 months.

-

Prepare collateral proof (land titles, purchase agreements, tenancy agreements).

-

Ensure your ID documents are up to date.

-

Keep debt levels manageable.

-

Savings culture - even small monthly savings build lender confidence.

You don’t need to be wealthy. You just need to be organized.

Common Mistakes to Avoid When Applying For A Loan

These mistakes cost African borrowers millions every year - and they’re completely avoidable:

-

Choosing the lowest interest rate instead of the most trustworthy lender

-

Not verifying land titles or ownership records.

-

Failing to budget for “hidden costs” (valuation, insurance, legal fees)

-

Taking short-term loans for long-term projects

-

Ignoring exchange-rate risks if earning in one currency and paying in another

-

Not reading the loan agreement carefully.

A smart borrower is a protected borrower.

Real Estate Loan Options in Cameroon and Across Africa

Here’s the truth:

Across much of Africa, traditional mortgages are scarce, slow, or difficult to access - especially for self-employed or informal earners. Cameroon is no exception.

But that gap has created something powerful:

Innovative housing finance solutions built for Africans.

Through BBOYO’s partnerships with lenders, cooperatives, developers, and alternative financiers, Cameroonians can now access:

-

Flexible mortgage-like Real Estate Loans

-

Diaspora home equity loans

-

Low-deposit construction support

-

Verified property listings backed by legitimate titles

-

Transparent terms, simplified documentation, and real human guidance

This is what modern African housing finance should be - clear, fair, culturally aware, and tailored to our economic realities.

And with the right knowledge and support, your dream property becomes not just possible, but achievable.

Conclusion

This is exactly where platforms like BBOYO step in - not as another middleman, but as a guide that helps you make sense of a market that often feels complicated from the outside. Through verified lenders, transparent terms, and support that speaks to our context - not copy-pasted from foreign systems - you get a clearer path, healthier loan options, and the confidence to take that next step.

If there’s one message to walk away with, it’s this:

You don’t need to be wealthy to own property. You just need the right information and the right partner beside you.

And once those two pieces fall into place, the dream of owning a home or investing in real estate stops being distant - it becomes a plan you can act on starting today.